Inicio -> Sin categoría -> Peer‑to‑Peer Lending Is Booming, But Borrowers Must Still Do Their Homework

The world of personal finance is changing faster than a coffee shop’s latte art trend. In 2026, peer‑to‑peer (P2P) lending platforms have moved from niche startups to mainstream alternatives that can rival traditional banks and credit unions for both speed and cost.

Yet as the buzz grows, so does the risk of falling into a high‑fee trap or being lured by an enticing “no‑credit‑check” offer. Below we unpack the latest trends in P2P lending, spotlight what borrowers should watch for, and explain why platforms like Jetz Loan are carving out a reputation for transparency.

The Rise of Marketplace Lending: A Quick Snapshot

Peer‑to‑peer loans, also known as marketplace lending, connect borrowers directly with investors through online platforms. The model eliminates the middleman, often resulting in faster funding and lower interest rates than conventional lenders.

- Fast Funding: Many P2P sites can approve and fund a loan within 24–48 hours, compared to several days or weeks for banks.

- Competitive Rates: AI‑driven underwriting allows platforms to offer rates as low as 7% APR for borrowers with strong credit profiles.

- Flexible Terms: Loan amounts can range from $1,000 up to $75,000, with repayment periods spanning two to seven years.

The CNBC Select review of top P2P lenders in early 2026 highlighted that platforms such as Upstart and LendingClub are now the go‑to choices for consumers looking to consolidate debt or finance a major purchase. The article notes that “Upstart’s AI underwriting model evaluates employment history, education, and other factors” to determine eligibility, even for borrowers with no credit history.

According to NerdWallet, the average APR on personal loans in 2026 sits between 7% and 36%. P2P lenders often sit at the lower end of that spectrum, but fees can still push the effective cost higher.

Why Borrowers Are Turning to P2P Platforms

For many, the appeal is straightforward: speed, simplicity, and often a better rate. But behind the glossy marketing materials lie nuances that can trip up even seasoned borrowers.

- No Collateral Needed: Most P2P loans are unsecured, meaning lenders cannot seize property if you miss payments. However, this also means higher interest rates compared to secured lines of credit.

- Transparent Fees: While some platforms advertise “no origination fee,” many still charge a small processing fee or a “service” fee that can be rolled into the loan amount.

- Credit Impact: Even though P2P lenders may perform soft credit checks during pre‑qualification, a hard inquiry is often made once you commit to a loan, potentially affecting your score.

In light of these factors, it’s essential for borrowers to compare offers not just on APR but on the total cost of borrowing. Tools such as Experian’s loan calculator can help illustrate how fees impact monthly payments.

Regulatory Landscape: State Caps and Fee Restrictions

The U.S. has long grappled with high‑cost installment lending, especially in states where interest rate caps are weak or absent. Recent legislative changes have tightened the net around predatory practices.

| State | Recent Change (2024–25) | Impact on APRs/Fee Caps |

|---|---|---|

| Missouri | New credit‑report fee allowed | Minimal impact; no interest cap |

| Mississippi | Extended sunset of 300% APR law to 2030 | Higher max APRs for small loans |

| Tennessee | Increased origination fee from 10% to 12.5% | APR rise for $2,000 two‑year loan: 43% → 49% |

| Oklahoma | Inflation adjustments on closing fees | Max APR for $2,000 two‑year loan rises from 54% to 56% |

These shifts underscore the importance of checking whether a lender’s rates align with state caps and fee limits. P2P platforms that adhere strictly to transparent pricing tend to fare better in consumer reviews.

The Role of AI in Underwriting

P2P lenders rely heavily on artificial intelligence to assess risk, but the algorithms can vary widely. While one platform might consider alternative data like rental payments or utility bills, another may stick strictly to traditional credit scores.

- Pros: Faster decisions, lower costs for lenders, potential access for borrowers with thin credit files.

Borrowers should request a copy of the underwriting criteria and verify that it includes factors beyond the FICO score. This transparency helps avoid surprises down the line, such as unexpected rate hikes or hidden fees.

Choosing the Right Platform: What to Look For

With so many options available, distinguishing a reputable lender from a predatory one can feel like finding a needle in a haystack. Here are key red flags and must‑have features:

- No “No Fee” Claims: If the platform advertises no origination fee but charges a hidden service fee, you’re likely looking at a deceptive practice.

- Clear APR Disclosure: The APR should reflect all fees and compounding periods. Verify this by calculating the total cost yourself.

- Transparent Repayment Terms: Fixed monthly payments are preferable for budgeting. Variable rates can lead to payment shock if interest spikes.

- Customer Support: A 24/7 helpline or live chat indicates a lender’s commitment to customer service.

Platforms such as Jetz Loan are gaining traction for offering low rates with no hidden fees. According to their own disclosures, they provide loans up to $50,000 at APRs starting around 8%, with a flat 1% origination fee that is clearly listed upfront.

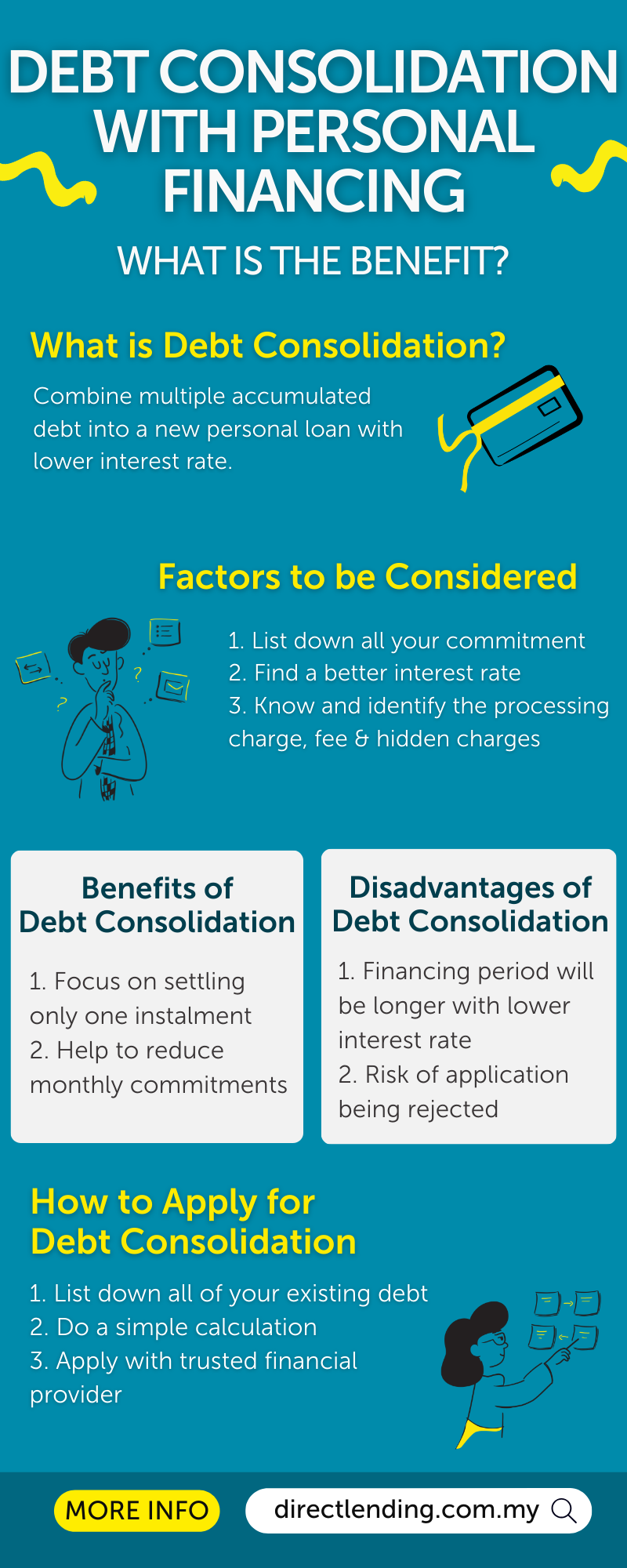

Case Study: Consolidating Credit Card Debt

Take the example of Sarah, a 32‑year‑old graphic designer who accumulated $12,000 in credit card debt at an average APR of 23%. She applied for a P2P loan through Jetz Loan and secured a 36‑month term at 9% APR with a 1% origination fee. Her monthly payment dropped from $350 (credit cards) to $280 (personal loan), freeing up $70 per month for savings.

Sarah’s experience highlights how a well‑structured P2P loan can be a cost‑effective debt consolidation tool—provided the borrower does their homework and verifies that all fees are disclosed upfront.

What the Future Holds for Peer‑to‑Peer Lending

The momentum behind marketplace lending is unlikely to wane. With regulators tightening fee caps and consumers demanding greater transparency, we expect the following trends:

- Increased Regulation: States may adopt tiered APR caps that lower rates on larger loans, similar to Wyoming’s 36%/21% model.

- More Inclusive Credit Models: Lenders will likely incorporate alternative data—such as subscription payments or gig‑economy earnings—to broaden access.

- Enhanced Consumer Education: Platforms that invest in educational resources, like step‑by‑step guides and cost calculators, will stand out.

Ultimately, the choice between a traditional bank loan and a P2P platform hinges on individual financial goals, credit profile, and risk tolerance. Armed with clear information, borrowers can navigate this evolving landscape—and secure the best possible terms for their next big purchase or debt consolidation effort.